We value a RIGOROUS risk management as an integral part of our GROWTH STRATEGY across all lines of business.

The group aims at a MODERATE RISK profile to ensure a BALANCED RISK and REWARD RELATIONSHIP within set risk appetite.

The Group embraces risk management as a core competency of its strategy to support business in delivering sustainable growth and help to reinforce its resilience by adopting a holistic approach to risk management. This is achieved by embedding a strong risk culture throughout the organisation and optimising risk-taking through objectivity and transparency.

The Group has a portfolio of fixed rate FCY assets mainly funded via floating rate liabilities. Foreseeing the rise in US interest rates, the bank has embarked onto new products like interest rate and cross currency swaps through the newly set up Derivatives Desk. This engagement will enable the bank to participate in higher yields from longer dated assets while being hedged with respect to interest rate changes.

The Derivatives Desk will also trade in credit default swaps, whereby the bank will earn income by taking credit exposure in investment grade entities, without actually trading the actual assets. Risk inherent to those new areas will need proper monitoring and control.

SBM has already kicked off the IFRS 9 implementation to ensure compliance by January 2018. With the implementation of IFRS 9, the provisioning level is expected to be higher than the requirements under IAS 39. The bank is currently leveraging all the required systems and process changes to support the strategic outcomes of the new regulatory requirement and enhancing its governance framework across data, models and reporting to incorporate IFRS 9 impairment models.

End-to end risk processes will be optimised to improve our service delivery in terms of customer on-boarding, loan disbursement, etc. In parallel we will increasingly leverage our new systems capabilities to come forward with innovative product offerings where risks need to be controlled.

In order to ensure that the alignment between the organisational and employees values leads to higher levels of commitment and engagement, a risk culture awareness exercise is being undertaken in 2017 to map the current risk culture to the desired future risk culture by identifying the gaps and areas for improvement and formulate a change strategy and specific initiatives on the best way forward.

On the technology front, the Group underwent a transformation in 2016 to refresh the technology platform and accommodate future business aspirations and geographical expansion in line with the strategies of the Group. 2017 will see continued focus on stabilisation of our new systems. Technology risk remains at the forefront of our focus.

The Group is conscious of the risk of cyber theft which has long replaced the «traditional» concept of bank robberies in many parts of the world. In light of the growing concern, the information technology risk management framework has been further enhanced in order to manage technology risks and safeguard information system assets in place. Physical security also remains important. The physical security policy has been enhanced to cater for additional controls and for the increasing role of the anti-fraud department and a dedicated physical security department which will be set up in 2017 to review all the security aspects of the Group’s premises. New measures are being put in place for cyber security to enhance resilience against cyber crime.

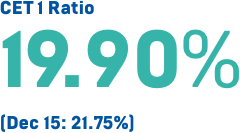

Tier 1 capital absorbs losses before other types of capital and any loss absorbing instruments. It includes ordinary shares issued and retained earnings and is capable of immediate use to cover risks or losses as soon as these occur.

Tier 2 capital is the supplementary capital and provides loss absorption capacity after Tier 1 capital. It typically consists of subordinated debt securities with a minimum maturity of five years.

| Dec-16 | Dec-15 | Dec-14 | |

|---|---|---|---|

| Liquid Asset to Deposits Ratio | 43% | 44% | 42% |

| Loans to Total Deposits | 69% | 69% | 75% |

| Loans to Total Funding | 63% | 65% | 68% |

| Liquidity Coverage Ratio (LCR)* | 116% | 133% | 118% |

| Net Stable Funding Ratio (NSFR)* | 125% | 107% | 101% |

* For Mauritius Operations only

Financial Publishing Solutions by NUMBERS